I published this alert last week for subscribers to my Trigger Event Trader VIP Trading Service.

However, I wanted to distribute the information to a wider audience because it’s important that all investors understand the risk that may be lurking in their portfolios.

I’m eager to know what you think. After you’ve read the whole thing, leave a comment and let me know whether this makes sense to you or I’m off my rocker (or maybe both!).

I’ve been very fortunate in my career in several ways.

One of the important ways is that I had a front-row seat to history and was old enough to realize it.

I didn’t jump into the market as a career right out of school. Instead, I was trying to be the next Alec Baldwin. However, I probably had the talent of Daniel Baldwin.

After a number of years, I gave up acting to begin a career in the markets. Shortly after, the dot-com bubble started inflating.

Though I still only had a few years under my belt, I knew how to read financial statements and understood that to be a successful business you had to have sales at the very least.

I also realized that the excesses of the dot-com bubble were not normal and were a sign of the top.

I knew the top was near when I attended a party celebrating a company’s new capital raise. How did they spend the precious dollars that investors trusted them with? By hiring James Brown (yes, that James Brown) and his band to put on a show for the 600 or so guests.

So as the AI bubble has inflated, I’ve kept an eye out for the companies that remind me of what I saw during those dot-com days.

And when the dust settles, we’ll look back and say it was obvious that Oracle (NYSE: ORCL) was going to crash.

This may be a surprising suggestion since Oracle is a real business, not at all like the dot-coms that measured their success by eyeballs instead of dollars.

Plus, the stock has been soaring over the past couple of days.

But Oracle has so overextended itself that its fall is almost inevitable.

Consider:

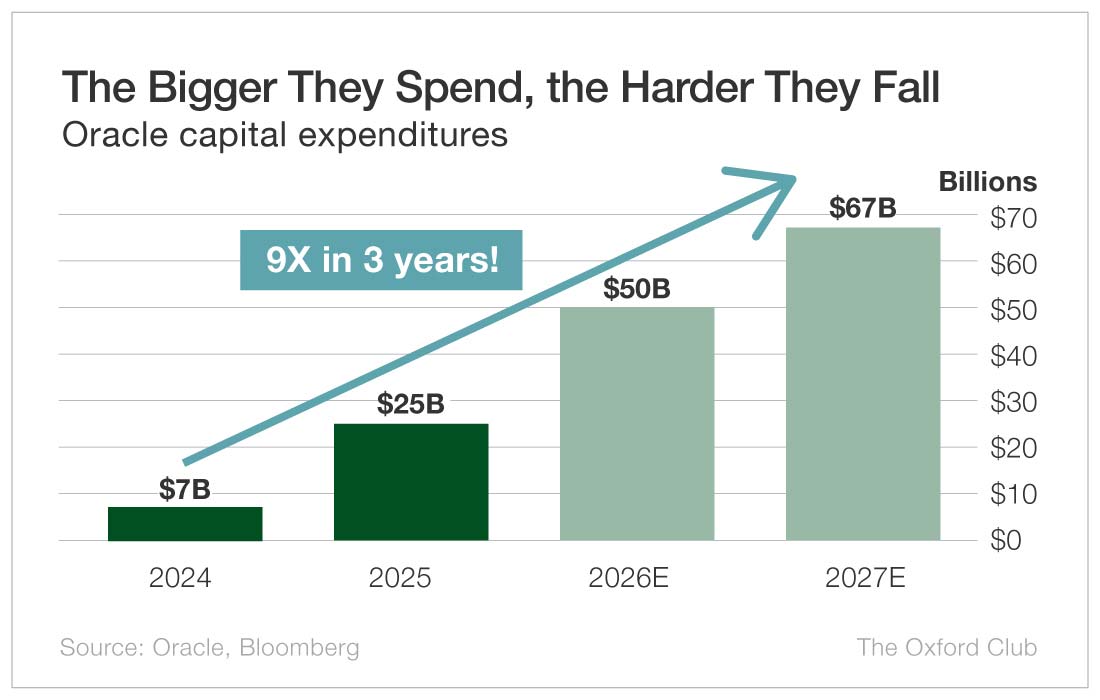

- Oracle’s capital expenditures are expected to rise from $7 billion in 2024 to $67 billion in 2027 as it builds out AI data centers – a more than 800% increase in three years.

- Free cash flow for this year is forecast to be negative $25 billion.

- Free cash flow for next year is forecast to be negative $26 billion.

- It has $125 billion in debt and $39 billion in cash.

So in order to pay for all of that capex, it must take on more debt or sell stock – both of which are negative for shareholders.

Last week, Oracle announced Hilary Maxson as the new CFO. Wall Street applauded the move, with one analyst saying Maxson was “built for capex.” In other words, spending money.

Funny, I’ve always wanted CFOs to be good at making money.

Again, after the stock implodes, we’ll look back and see that comment as something ridiculous you say at the top.

But here is what nobody is talking about.

Oracle has $250 billion in off-balance sheet obligations.

In other words, a quick glance at its financial statements doesn’t show the true amount that Oracle is on the hook for.

Much of this $250 billion is for leases that Oracle is contractually obligated to pay for even if it decides it no longer needs the space.

On the other hand, $300 billion in future revenue is from a single customer – OpenAI, the company behind ChatGPT.

ChatGPT is losing ground to Google’s Gemini and X’s Grok. If ChatGPT is not able to meet its obligations to Oracle, then Oracle has a big problem.

Perhaps the canary in the coal mine is that Blue Owl, a large lender to businesses, including Oracle, pulled out of a deal to finance more data centers.

Everything has to go nearly perfectly for Oracle’s finances to recover.

But there’s one more thing that could affect the stock and has nothing to do with Oracle’s business.

The Paramount-Warner Brothers deal also has to go perfectly.

Paramount’s CEO is nepo-baby David Ellison, the son of Oracle founder and chairman Larry Ellison.

Papa has personally backed the Paramount acquisition of Warner Brothers to the tune of $40 billion.

Larry Ellison is quite wealthy, but he probably doesn’t have billions sitting in cash. If the deal runs into trouble, Ellison will likely have to sell Oracle shares in order to fund his son’s new toy.

What happens when news breaks that Larry Ellison is selling?

Shorts will pound the stock, sending it lower and ensuring he has to sell more in order to come up with the cash for the deal. That’s what hedge funds do.

Other holders will bail, trying to get out before Ellison is done selling. After all, you can’t just dump a few billion dollars’ worth of shares at once.

I expect the stock to trade down to $125 in the near term.

Longer term, I suspect it will go to $50 and, if things really get nuts, to $20.

Owners of Oracle shares should consider taking defensive measures such as a stop or buying longer-term puts. Speculators can consider longer-term puts as well.

When the AI bubble eventually collapses, a number of companies will be buried in the rubble.

Oracle will be one of them.

can you explain how a person can benifit if a stock is declining in price? is shorting the only way to go?

Mark, as always, thanks for your insight.

Hi Marc,

I think you are dead on. I’m 74 years old and lived in NYC for 40 years before retiring to Spain three years ago. So, I’ve been around the rodeo. As a retired person, I have Paramount Bonds in my portfolio. How safe do you consider them, and should I be selling?

Thanks for all you do for us.

What is ‘near term’ in your mind?? To ME, it means less than 3 months. August 21 125 puts are 6.00 a contract!! NOT exactly something the average retail trader can afford. I mean, yeah, if it drops to 100 before then, you make a F#$%ton of money, but * I * don’t have 6 grand just laying around!! July 17th is 4.43. (I don’t have $4400 laying around, either!) I thought you were looking to help the ‘little guy’ make money in the markets. 5k in ‘spare cash’ is NOT ‘the little guy’!! I paid for your service for several years, but SO many of your trades are just not feasible for MOST people!!

Hi B. Dodds, we hear your concern about making our recommendations accessible to everyday investors – that’s something that’s very important to us that we’re constantly keeping in mind. However, please note that an option that’s priced at $6 per share will cost $600 per contract, not $6,000, and one priced at $4.43 per share will cost $443 per contract, not $4,430.

Don’t worry Marc you’re not off your rocker at all. Honestly, the debt, capex and dependence on one customer are enough to make anyone nervous.

That said, I would not short Oracle right now. In this market, logic seems to have taken a vacation and left the interns in charge. We’ve seen plenty of stocks keep going up long after everyone agrees they should not.

Could Oracle eventually become one of the poster children of the AI bubble? Absolutely. But trying to time that is like standing in front of a train because you are convinced it will eventually run out of fuel.

In this market, “too expensive” and “makes no sense” are sometimes exactly the reasons a stock goes up another 50%.

First, I don’t know anything about anything. But if you owe more than you have coming in for the next two years, and two huge deals have to go perfectly, at least one of them won’t. Just like throwing a pass in football has three possible outcomes, two of which are bad, I don’t like those odds either.

Beg to differ. While not caught or intercepted are bad, plus offensive pass interference is bad there are 2 good possible outcomes. They are that the pass is caught or a penalty on the defense – either pass interference or holding. And they are more likely than the bad ones. That said, the premise that capex far exceeding income plus the need for 2 huge deals to go perfectly is definitely bad. However, we can’t yet define a time frame for it to play out. Right now the Iran war is still ongoing yet the S&P set a new record high today and NASDAQ is knocking on the record door. Until indicators show the market in general and ORCL in particular have topped out, it’s dangerous to bet against them. I confirmed that yesterday with 2 bear call spreads that lost me about $2700. The old saying that the market can remain irrational longer than you can remain solvent is especially true in the current crazy market.

Marc- thanks for update. I took your advice from last week and shorted ORCL @ 145 – and watched it go to 165. Ouch! How much pain are we supposed to take before your prediction comes true? Kind regards.

Thanks for the insight Marc. Fundamentals might not matter on the way up, but they suddenly do on the way down. Sounds like it will be a great short at some point. I’ll wait for your alert!

I’ve gotta admit. I was surprised at the information. But, that’s the kind of information I appreciate from your subscriptions. Thanks for your input. Thank God, I don’t own Oracle