Entergy (NYSE: ETR) sits in an interesting position – despite operating a dull business within a market that still cares about rates and cash flow.

The company is a regulated electric utility. It generates, moves, and sells power to more than 3 million customers in Arkansas, Louisiana, Mississippi, and Texas. Its main work is power delivery, grid investment, storm recovery, and service to homes, businesses, and heavy industry across the Gulf South.

It serves a region where power demand is growing, but it must keep spending heavily to support that growth. That tension matters more than meets the eye, because a utility can have a sound business case and still carry a price that leaves little room for weak cash flow.

In the first quarter of 2026, Entergy’s revenue was $3.2 billion – up 12% from $2.8 billion a year earlier. Net income was $384.9 million, an increase of 6.7% from last year’s $360.8 million. Operating cash flow was $829 million, representing growth of more than 54% year over year.

Power use was also higher. Total retail power sales came in at 30,737 gigawatt-hours, up 4.5%. Weather-adjusted retail sales rose 6%, and industrial volume rose 14.9%.

Entergy paid $292.9 million in common dividends during the quarter. It had $7.9 billion in gross liquidity, which means it had a healthy amount of cash and credit available.

Investors have been giving Entergy the benefit of the doubt. The stock’s recent move points to steady confidence, and that fits the stronger demand data.

The risk is that the price may be based on an assumption that cash flow will improve.

Now to The Value Meter.

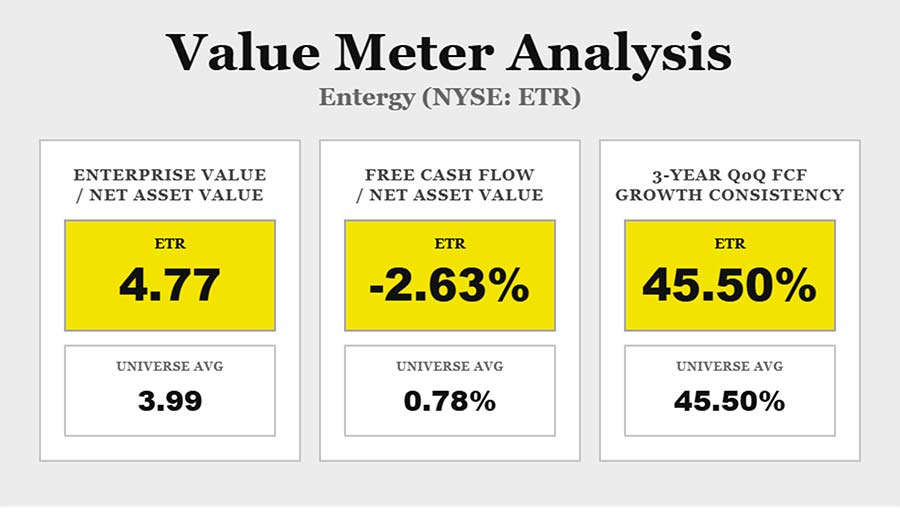

Entergy’s enterprise value-to-net asset value (EV/NAV) ratio is 4.77, versus the broad market average of 3.99. That is about 20% higher, so investors are paying more for each dollar of Entergy’s assets.

The company’s free cash flow-to-net asset value (FCF/NAV) is -2.63% over the past 12 months. The broad market average is 0.78%, so Entergy is lagging well behind its peers on this measure.

That tells us that the company’s assets are not producing strong free cash flow yet. Heavy utility spending can explain part of that weakness, but it still makes the valuation less forgiving.

Entergy’s three-year quarter-over-quarter free cash flow growth consistency is 45.5%, the same as the broad market average. The company has not shown better cash flow progress than the market, even though the stock carries an above-average asset valuation.

The market appears to be assuming that stronger power demand will turn into better cash flow over time. That may happen. But today’s numbers show a stock priced above the market on asset value with weaker free cash flow and no edge in cash flow consistency.

This is not a bad company. It’s a good utility with a price that’s already giving it credit for improvement that hasn’t happened yet.

In other words, Entergy is not weak. It’s priced with little room for error.

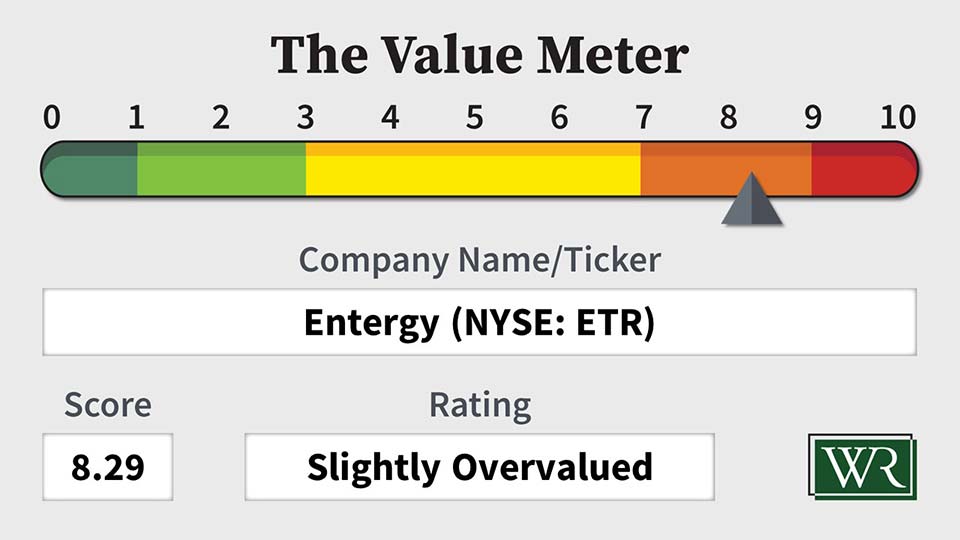

The Value Meter rates Entergy as “Slightly Overvalued.”

What stock would you like me to run through The Value Meter next? Post the ticker symbol(s) in the comments section below.

shw clx

Asts

WMB

NewtekOne would be interesting

Kind regards Martin

Hi Anthony,

Very interesting assessment as always.

In a similar vein, I would love to hear your thoughts on Vistra Energy.

It had a tremendous run-up over the past five years or so. I’m curious if you consider it fairly valued at this time.

Thanks,

Richard

Target or HP

HNHPF

Am interested in the value meter rating for SFTBY

VZ