Editor’s Note: The stock Director of Trading Anthony Summers evaluates in this week’s Value Meter is a fitting choice to end our “America’s 250th Birthday” series. (You’ll see what I mean below.)

If you missed any of the previous articles in the series, check them out here:

- “What Makes America Great” by Chief Investment Strategist Alexander Green

- “A Lesson From 1973” by Macroeconomic Strategist Dr. Mark Skousen

- “The Heart and Soul of America” by TrendLabs Founder JC Parets

- “The Next Iconic American Companies” by Chief Income Strategist Marc Lichtenfeld

There will not be a new issue of Wealthy Retirement tomorrow. We’ll return to our normal schedule on Sunday with your weekly recap.

From our entire team, wishing you and your loved ones a happy Independence Day.

– James Ogletree, Senior Managing Editor

Tomorrow, America turns 250.

There will be fireworks, flags, and, in plenty of coolers, beer.

Few beer brands lean harder into the American story than Boston Beer (NYSE: SAM). Its flagship brand is named for Samuel Adams, a Founding Father and signer of the Declaration of Independence. Its first Boston Lager was brewed in the 1980s, and the company helped push American craft beer into the mainstream.

I still remember enjoying Sam Adams Cherry Wheat for the first time back in college, well before time and experience drew me toward aged scotch and medium-bodied maduro cigars.

(A man has to start somewhere…)

But Boston Beer is no longer just a Sam Adams story. The company now makes Samuel Adams, Twisted Tea, Truly, Angry Orchard, Dogfish Head, and Sun Cruiser. Its portfolio includes hard tea, hard seltzer, cider, and ready-to-drink alcoholic drinks − not just beer.

That’s a broad lineup, but Boston Beer is still fighting for consumer attention.

In the first quarter of 2026, net revenue fell 4.4% from $453.9 million a year earlier to $433.9 million. Depletions (the amount of product moving from distributors to retailers) fell 4%, and shipments fell 6.9%.

The company lost $145.3 million during the quarter after earning $24.4 million a year earlier, but that loss was skewed by a $216 million litigation charge tied to a supplier dispute. That is real money, but it is not the same as a normal operating collapse.

There was some progress too. Gross margin rose from 48.3% to 49.3%, which means Boston Beer kept more profit after product costs even while sales fell. The company also ended the quarter with $164.1 million in cash and no debt.

Despite that, the market still does not love the stock.

But is the market punishing Boston Beer fairly… or too much?

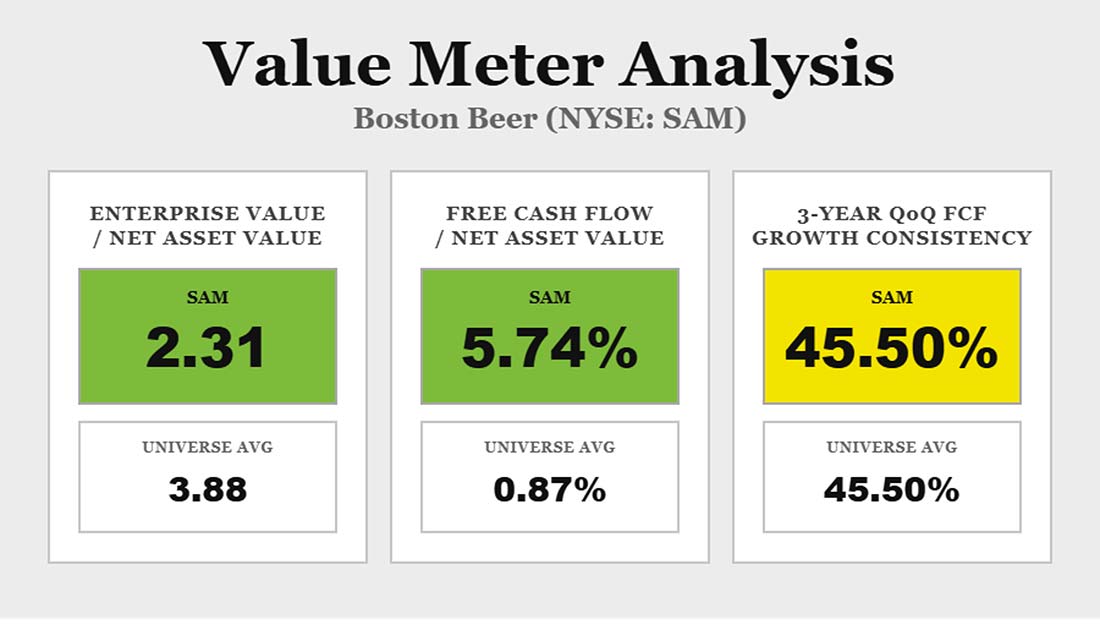

The first useful test is what investors are paying for the business versus its net asset value. Boston Beer’s EV/NAV is 2.31, versus a broad market average of 3.88. In other words, the company’s EV/NAV is about 40% lower than the broad market average.

That does not make the stock a bargain by itself, but it does show that investors are paying much less for Boston Beer’s assets than they are for the average company’s.

The cash flow test is stronger.

Boston Beer’s FCF/NAV is 5.74%, approximately 6 1/2 times higher than the broad market average of 0.87%. Over the past three years, its quarterly free cash flow has grown over the previous quarter 45.5% of the time, which is in line with the market average.

Basically, Boston Beer looks cheap on asset value and strong on cash flow, but it has not yet shown steady enough demand or cash growth to make it a screaming buy.

That being said, the stock may deserve more attention than the market is giving it.

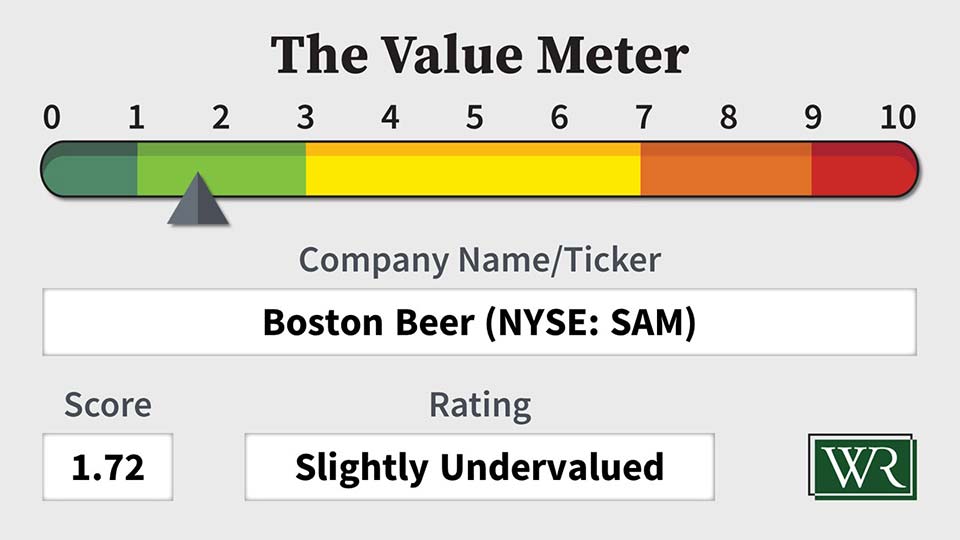

The Value Meter rates Boston Beer as “Slightly Undervalued.”

What stock would you like me to run through The Value Meter next? Post the ticker symbol(s) in the comments section below.