“This will be good for Susan,” the man told my uncle.

My cousin Susan was 8 years old at the time. My uncle’s best friend had recommended an investment, one that he had already put his own money into. For $15,000, my uncle could join a partnership in an office building on 39th Street and 1st Avenue in Manhattan.

This conversation took place more than 60 years ago, so $15,000 was a large sum.

My uncle was not in the habit of throwing money around without a lot of thought. He came from a poor family and had worked too hard since he was 14 years old to be frivolous with his cash.

The friend was a successful businessman, so my uncle trusted him and followed him into the partnership.

The friend was right. It has been very good for Susan. Today, Susan earns $48,000 a year in income from that partnership – more than a 300% annual yield on my uncle’s original investment.

A 60-Year Horizon

Susan is retired now. A former teacher, she has a decent pension with solid benefits. Does that extra $48,000 come in handy? You bet it does. She and her husband recently took a monthlong cruise to Europe. Their house is paid for, and they can easily handle the cost of long-term care insurance so as not to burden their children should they get sick.

They live well thanks, in part, to my uncle’s $15,000 investment in 1953.

The money didn’t always belong to Susan. My aunt and uncle collected the income annually from the partnership for more than 50 years. But they never sold it because they knew it would eventually be “good for Susan.”

Very few of us have a parent or role model who looked so far into the future. As a result, we do not have an investment horizon of 60 years.

But we all have a few Susans in our own lives – loved ones who could benefit from our investment skill, but not until we’re finished with the investment ourselves.

It might be six decades too late for you to get in on that Manhattan office building, but there are plenty of investments out there that will pay you a rising income annually, while generating a ton of cash years down the road.

How to Do It

My favorite way to set up this scenario is with Perpetual Dividend Raisers – stocks that raise their dividends every year.

That’s because by lifting the dividend every year, management sets the bar very high.

Imagine what would happen if, after six decades of annual dividend increases, American States Water (NYSE: AWR) did not hike its dividend. As Ricky Ricardo from I Love Lucy might say, the CEO would have “some ‘splainin’ to do!”

A CEO who does not raise the dividend after a long streak should probably get their resume together. Investors have come to expect annual dividend increases in these companies, and management teams work very hard to be able to provide them. If, after 20 or 30 years, dividend boosts suddenly come to a halt, that would suggest a drastic change in the company’s business or prospects.

If you’re reinvesting your dividends, owning Perpetual Dividend Raisers helps you step on the gas of the compounding machine.

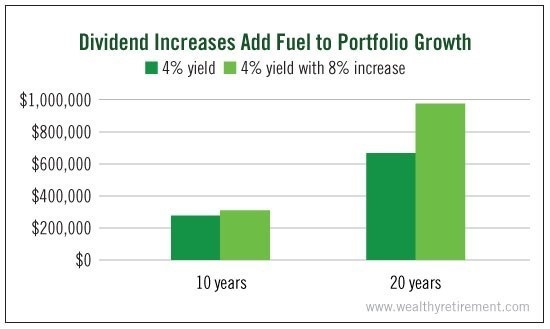

Let’s say you have a $100,000 portfolio of dividend stocks with an average yield of 4% and it climbs by the historical average of the S&P 500 – and you reinvest the dividend.

After 10 years, your $100,000 will be worth $278,544, and you’ll receive about $5,300 per year in dividends.

After 20 years, your nest egg is worth $668,103. And the portfolio spins off $6,100 per year in dividends.

Not bad, right?

But what if instead of earning a flat 4%, your portfolio starts off yielding 4% and the companies average an 8% dividend boost every year? The numbers increase significantly.

In 10 years, you have $310,764… $32,000 more than the first scenario. More importantly, you’re now generating $11,780 in dividends, more than double what you would have made if the company did not boost the payout.

In 20 years, the portfolio is worth $978,406 – a whopping 46% more than the earlier case. And if at that point you’re ready to stop reinvesting the dividend and take it as income, you’ll receive $38,290. That’s a far cry from the $6,100 you’d get without the dividend increases.

That will be very good for your Susan.

Perpetual Dividend Raisers are a great way to get some income today and an even larger “paycheck” for your heirs later.

Good investing,

Marc