Editor’s Note: Today’s guest article comes from JC Parets, a Chartered Market Technician and the Founder of TrendLabs.

JC’s stated mission is “to decode market behavior using pure technical analysis to reveal the truth behind every move.” I met him personally at our Investment U Conference in Las Vegas in March, and I was impressed by his clear, no-nonsense approach.

I learn something every time I visit TrendLabs’ website, and I think you will too. Go here to check out the latest insights from JC and his team.

– James Ogletree, Senior Managing Editor

- I love bubbles and I wish we had more of them.

- There’s a difference between excessive optimism and disbelief.

- There’s a bubble in people calling things bubbles.

One of the biggest mistakes investors make is forgetting the most important characteristic of asset prices:

They trend.

Not sometimes. Not when the Fed says so. Not when valuations look attractive. Just structurally, over time, asset prices trend.

We’ve got more than 150 years of market history showing us the same thing over and over again. Stock prices are not random. Trends persist much longer than people think they should.

Which is why I’ve always found it funny when smart people refuse to participate in a market uptrend because they think it’s a bubble.

Wait a minute.

If you genuinely believe you’re looking at a bubble, shouldn’t you want to own it?

George Soros famously said, “When I see a bubble forming, I rush in to buy, adding fuel to the fire.”

That wasn’t some reckless gambling mentality. It came from his theory of reflexivity, the idea that rising prices themselves can change behavior, attract more capital, and push prices far beyond what anyone thinks is reasonable.

And it worked out pretty well for him.

Soros founded the Quantum Fund in 1970 with just $12 million and turned it into roughly $25 billion over the next three decades, compounding at around 30% annually along the way.

That kind of track record doesn’t come from sitting around waiting for things to “make sense.”

This is also the same guy who famously shorted the British pound in 1992, nearly broke the Bank of England, and made a billion dollars in a single day.

In other words, this wasn’t some tourist talking.

What’s important is that Soros understood something most investors still struggle with today: Bubbles are powerful trends.

They are not environments where you sit around hiding in cash, angrily waiting for the world to finally agree with you.

In fact, being early calling the end of a bubble can be financially devastating.

Ask the people who spent years shorting tech in the late 1990s. Or Bitcoin every year since 2013. Or stocks basically any time they make new highs.

As Jason Shapiro said this week, “Being short a bubble sucks.”

Honestly, that quote says more about market behavior than most finance textbooks ever could.

Because here’s the funny part: I don’t even think this is a bubble.

A Bubble in People Calling for Bubbles

Here’s the problem with all the bubble talk.

If everybody thinks we’re in a bubble, then by definition we probably aren’t.

Go study every major bubble in history.

The Dot-Com Bubble. The Roaring ’20s. Railroads. The South Sea Bubble. Even the Great Bowling Bubble of the 1960s.

What do they all have in common?

Euphoria.

Not fear. Not skepticism. Not constant debates about crashes and valuations and recessions every single day on television and social media.

Real bubbles happen when people stop believing risk exists.

That’s the part everyone forgets.

My friend Joe Fahmy said it perfectly this week: “There’s a bubble in people calling for bubbles.”

He’s right.

In actual bubbles, investors become convinced prices can only go higher. Every dip gets laughed at. Risk management disappears. People start believing we’ve entered some new permanent era where the old rules no longer apply.

Do you honestly see that today?

Just before the recent rally, individual investors were bearish on stocks over the next six months in 10 of the previous 11 weeks.

Consumer Sentiment just hit fresh all-time lows this month. More than half of American adults believe now is a bad time to invest in stocks.

Does that sound like euphoria to you?

Because to me, it sounds more like disbelief. And that’s an important distinction.

Because bubbles are built on optimism.

Bull markets climb walls of worry.

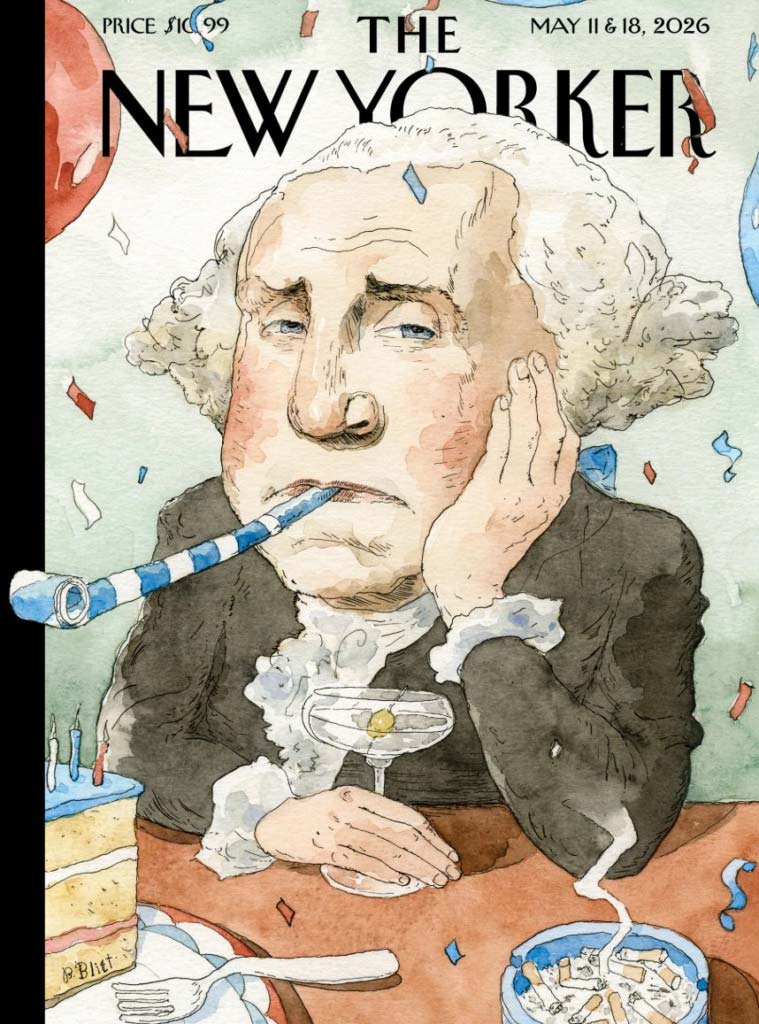

“Red, White & Kinda Blue”

Here’s what I keep coming back to.

The S&P 500 and the Nasdaq 100 just closed at fresh all-time highs again. These are the two most American stock indexes on Earth.

And this is the cover image a major magazine decides to run?

The headline literally says, “Red, White & Kinda Blue.”

Now look at George Washington.

Does that look like a guy caught up in speculative mania? Does he look euphoric?

The poor guy looks absolutely miserable. Honestly, that’s exactly what the sentiment data has been telling us.

Consumers are pessimistic. Investors are skeptical. Americans are overwhelmingly convinced something is wrong, even while stocks continue to trend higher.

That is not what bubbles look like.

Bubbles happen when people feel invincible. When everyone thinks getting rich is easy. When risk stops mattering and nobody can imagine stocks ever going down again.

I don’t see any of that.

I see disbelief.

And if this actually were a bubble, we’d probably want to own a lot more of it.

I love bubbles. I wish we had more of them.

But this just isn’t one. This is just a regular bull market doing regular bull market things.

And considering we’ve already lived through a historic crash, a vicious bear market, and multiple double-digit corrections in just the first half of this decade, I’m not really sure what people were expecting.

Another collapse already? How many more do they need before they finally believe the trend?

There’s a bubble in people calling things bubbles.

And remember, being short a bubble sucks.

Being short a bull market usually sucks, too.

JC,

I watched a bubble build in 1999. Dot coms were created out of thin air with no money behind them. Companies were created out of thin air. Wall street brokers were pushing garbage on people who did not take the time to do their homework. AI is the next Great Frontier like Vanderbilt who built railroads, Carnegie who built steel mills to build steel framed skyscrapers, and John D. Rockefeller who had the vision to provide gasoline to Henry Fords Model T’s. Roads were paved to allow Americans to experience the great outdoors, National Parks, and get on the road to explore and experience the country. The great pioneers of America did not pay taxes so it was easy to build Mansions on the Noth Shore of Long Island, and summer houses in Newport. As a well read 66 year old, my father was a WW 2 Tank Commander under Patton. Survived many battles, came back to Long Island and with the GI -Bill, bought a home and raised a family. That was a 75 year boom From railroads to the 60’s and lots of prosperity. Then Apple 2E came, IBM and their mainframes, before Dell, and Compaq with Microsofts software to drive these new machines which launched us into the Computer age. The internet was the next jump but the time between all these new innovations was much smaller. Here we are now. I was a printer and binder and software Packaging Sales Executive for 40 years before the Cloud took everything digital and sucked it up. The AI Revolution is the next thread in mankind’s jump to the next stage of life, and existence. My Grandfather lived thru the Great Industrial Revolution, my father a WW 2 Vet worked in the Publishing Business manufacturing books for Education, a depression kid created a Baby in the Boom years – (me). Now us Boomers are experiencing the next Information superhighway cloud based distribution of content. The Great depression taught us that 10c on the dollar to buy a share of a companies’ Stock was far too much levered paper and as a result, we had a crash. No money behind the paper. Bank runs, and not enough cash to cover all that paper stock. The crash of 2000 was no different. Dot Com companies created out of Thin Air. Many people lost money. Companies like Lucent Technologies, Texas Instruments, and Cisco were way over valued based upon PROFITABLE CASH FLOW. Today, Companies like Google, Netflix, Amazon, Microsoft,

are building the next railroad train tracks for AI to ride on hence vaulting us to another new Sphere of life. The Difference is the CapEx spent is with profits earned, not debt with the hopes or recouping. Any company levered super high to me is in that imaginary bubble. My advice to others (which I preach to my 2 sons) is invest in what you know. If you don’t know, then do your research, homework, and understand what the company does and how it will contribute – to THE AI Build out, and CAN IT BE SUSTAINED!!!!!!

Nothing wrong with take profits off the Table as well. Example: I buy 500 shares of Micron Technologies for $50.00 a share several years ago. Now at $650.00 a share. So we sell 250 shares at $350.00/share in our IRA, reload our cash position by $105,000 and have Gunpowder to buy into a great company when there is a huge down turn, Buying into a downturn is nothing more than dollar cost averaging over a 30-50 year period. I SAY TO YOUR AUDIENCE – Be patient, read about a company and what they can contribute to the future Super highway of information, and know that the product or service they offer is needed and can be sustained for a long PERIOD OF TIME.

MR. ETTINGER

You r a smart man. Thank u for sharing your insights. Many lessons to b learned if one is willing to pay attention.