There are two kinds of businesses that are challenging to value outright.

The first are banks. The second is the focus of this week’s column.

Biotech firms more often than not can look like make-believe businesses. Many have no major product on the market and no clear path to profit.

Yet they can still draw huge interest from traders.

The market’s attention may center on a new drug candidate, it may focus on a clinical trial, or it may revolve around a trailblazing development method that could reshape the industry years from now.

No matter the story, the story alone can drive the stock.

Grail (Nasdaq: GRAL) is different.

The company is built around Galleri, a blood test designed to find many kinds of cancer early. The story here is simple to explain: Galleri aims to find cancer sooner, when it may be easier to treat. If successful, that would mark a major shift in care.

Today, many cancers still have no standard screening test. According to Grail, more than 70% of cancer deaths come from cancers without standard screening.

As potentially transformative as Galleri is, the company’s financial position deserves just as much attention.

In the first quarter of 2026, the company posted a net loss of $93.2 million and a gross loss of $14.3 million. However, the trend looks better than the raw losses suggest.

First quarter revenue rose 28% from the prior year to $40.8 million, and Galleri revenue rose 37% to $39.8 million. Test volume increased 50% to more than 56,000.

Even the losses moved in the right direction. Net loss improved by 12%, gross loss improved by 28%, and adjusted EBITDA – earnings before interest, taxes, depreciation, and amortization – shrunk by 19% from -$99 million to -$80 million.

The company also has a notable amount of cash on hand. It ended the first quarter with $823.1 million in cash, cash equivalents, and short-term marketable securities.

For a biotech firm, that matters even more. Cash buys time, and time is often the difference between a strong idea and a failed one in this industry.

Given that the company submitted its premarket approval application for Galleri to the FDA in January 2026, time is exactly what it needs most. (The application remains under review.)

After a mostly uninspiring year in 2024, the stock roared in 2025, more than tripling from January to February and doing so again from August to the end of the year.

Since then, however, it’s fallen from a high above $115 to its current price around $62.

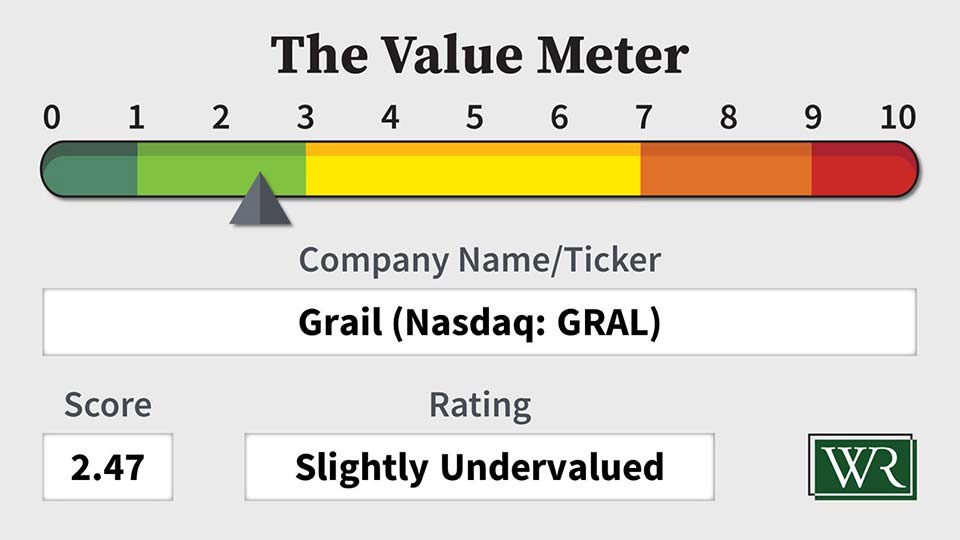

Now comes the real question: Where does The Value Meter land in all of this?

The answer may surprise you.

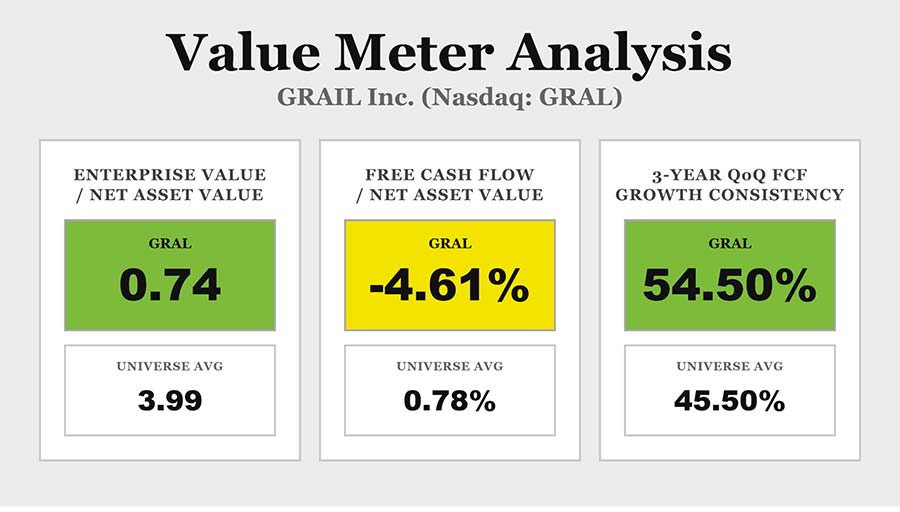

Grail’s enterprise value-to-net asset value ratio is 0.74. The broad market average is 3.99. That means the company trades at a large discount to the market on this measure.

That is the strongest point in its favor.

The weakest point is free cash flow. Grail’s trailing 12-month free cash flow-to-net asset value ratio is -4.61%. The broad market average is 0.78%.

The company is not yet producing cash. It is still consuming it.

But the third measure adds balance.

Over the past three years, Grail’s quarter-over-quarter free cash flow improved 54.5% of the time. The broad market figure is 45.5%. That means the cash flow trend has been steadier than the market median.

For a company at this stage, that matters.

Of course, there are still many open questions that should give investors pause.

The stock could fall sharply if data disappoints or if FDA review takes longer than expected. Adoption could also be slower than investors hope, and cash burn could rise again.

Still, the setup here is not entirely built on imagination.

Revenue is growing. Test volume is rising. Losses are easing. The balance sheet gives the company room to operate, and the valuation remains low relative to net asset value.

That mix is rare in biotech – rare enough to make me think this is more than just a good story.

The Value Meter rates Grail “Slightly Undervalued.”

What stock would you like me to run through The Value Meter next? Post the ticker symbol(s) in the comments section below.

RXRX please. One from Alex !

Gap

OHI and MO and EPD and UTG and UTF how safe are their Dividends?

Bloom energy

I have been President’s Circle for a long time. I think Anthony has matured into a masterful, intriguing writer. His value meter thing is specific and kind of fun. You go Anthony

Please run DXYZ through the value meter.

Sats