Over the past two decades, a handful of web browsers have come to define the internet for most people.

Chrome. Firefox. Safari.

But those are not the only browsers in town. They aren’t the only ones making money, either.

That is the setup for Opera (Nasdaq: OPRA), the company behind the Opera and Opera GX browsers and their newer AI tools. Opera gives users desktop and mobile browsers and then earns money from ads and search activity tied to that audience.

At first glance, that can seem like an old internet name trying to dress itself for the AI age. But the latest numbers suggest the case is more than spin.

In the first quarter of 2026, revenue rose 23% to $175.8 million. Net income rose 36% to $24.8 million, and operating cash flow rose 164% to $42.1 million.

Opera had 288 million average monthly active users during the quarter. That is a large base. The company is also getting more out of that base, with average revenue per user up 25% from a year earlier.

The market has not ignored Opera. Since its low earlier this year, the stock has done very well. But against the backdrop of the past couple of years, investors seem more uncertain and cautious than excited.

That brings up a useful question: Is the stock still cheap enough to deserve attention, or has the better case already been priced in?

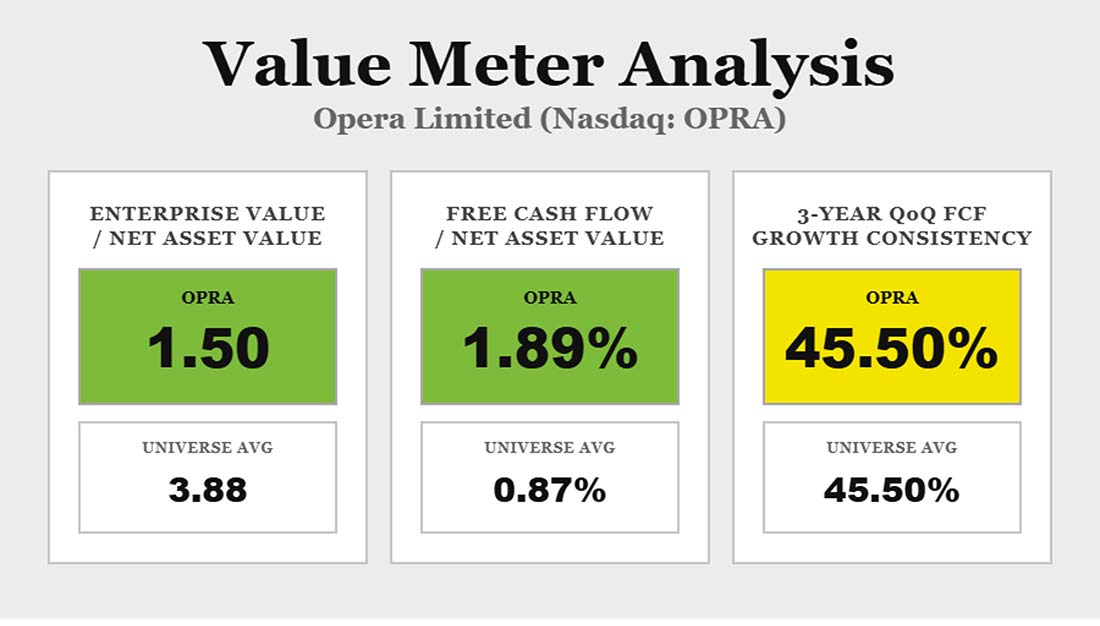

The first test is what investors are paying compared with the company’s net asset value. Opera’s EV/NAV is 1.5, versus a broad market average of 3.88, so its EV/NAV is about 61% lower than average.

That means investors are paying less for each dollar of Opera’s net asset value than they pay for the average stock. On this measure, Opera looks cheap.

The next test is cash flow. Opera’s trailing 12-month FCF/NAV is 1.89%, about 118% higher than the broad market average of 0.87%.

That is the stronger part of the case. Free cash flow is the cash that’s left over after basic business needs, and Opera is producing more of it relative to its net asset value than a typical company.

Over the past three years, Opera’s quarterly free cash flow has grown over the previous quarter about 46% of the time. The broad market average is also about 46%. Though the cash flow is good, it has not been unusually steady.

That keeps the rating from being stronger.

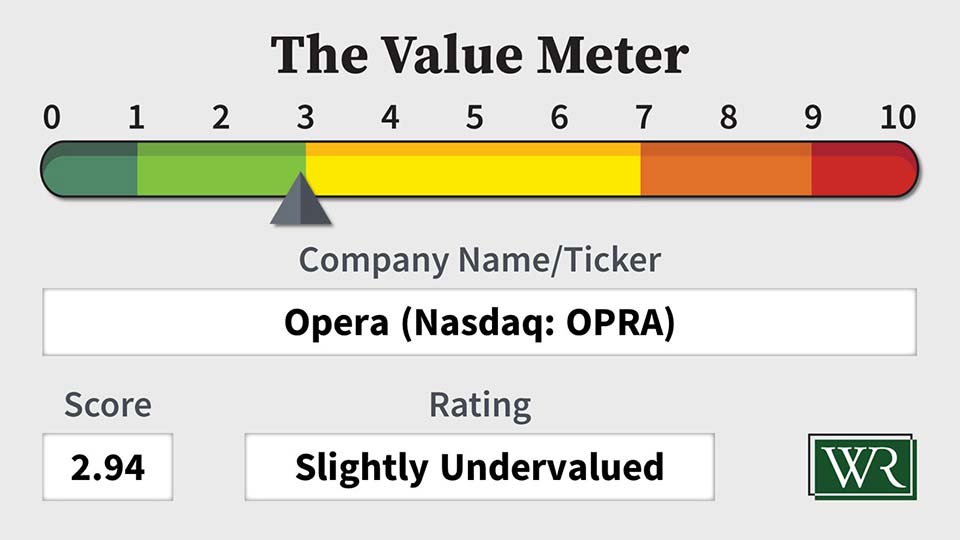

Opera’s case has improved more than its recent stock action suggests. The stock looks cheap on asset value and strong on cash flow.

The Value Meter rates Opera as “Slightly Undervalued.”

What stock would you like me to run through The Value Meter next? Post the ticker symbol(s) in the comments section below.