Back in July, I covered Flowers Foods (NYSE: FLO) in one of my Safety Net columns. At the time, it had been falling for 2 1/2 years and had lost half its value. But the 6.3% yield was tempting to some investors, so we dug in to determine whether it was safe.

The stock earned an “A” rating for dividend safety.

Since then, the dividend has stayed flat… but we can’t say the same for the stock price. It has continued to slide, falling another 47%.

Because of the price decline, the yield now stands at an eye-popping 12%.

Is it still safe?

Flowers Foods is the second-largest producer of packaged bakery goods in the United States. It was founded in Thomasville, Georgia, in 1919 and now has more than 10,000 employees in 19 states.

Its brands include Nature’s Own, Dave’s Killer Bread, Wonder Bread, and Tastykake.

The company has been seeing lower volume and losing market share for several years as higher prices have put pressure on consumers, leading them to cheaper, private-label store brands.

Despite declining market share, free cash flow has actually held up quite well – until now.

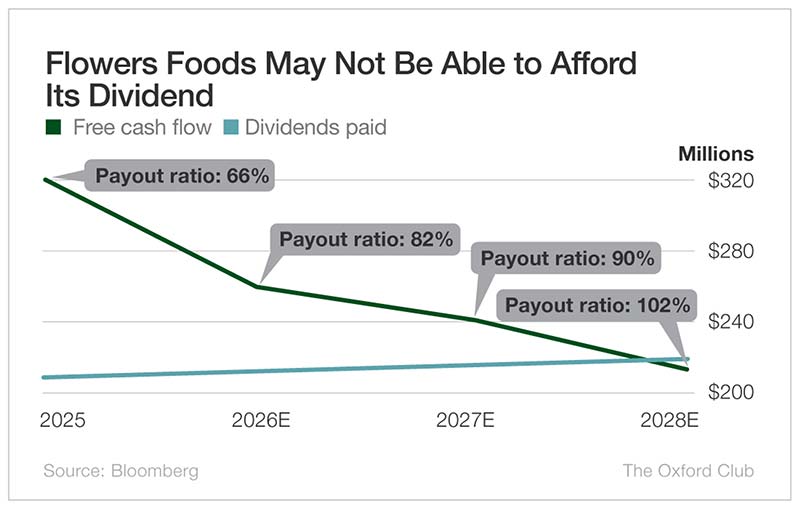

After four years of growth, free cash flow is forecast to decline in each of the next three years.

Last year, Flowers Foods paid shareholders $209 million in dividends, which was 66% of its $319 million in free cash flow.

That’s fine. I want to see a payout ratio of 75% or below to feel confident that the company can continue to pay its dividend even if free cash flow hits some obstacles.

This year, however, the payout ratio will cross that threshold and come in at 82% if Wall Street’s projections are accurate.

In fact, according to analysts, by 2028, the dividend will surpass free cash flow.

Falling free cash flow and a too-high payout ratio are both problematic.

One thing Flowers Foods has going for it is its dividend-raising track record.

The company has raised its dividend in each of the last 23 years. However, it typically boosts the payout in the first quarter and didn’t do it this year.

The current quarterly dividend is $0.2475, which comes out to a 12% yield.

That impressive track record of annual dividend raises earns Flowers some grace from the Safety Net model, but the model does have to penalize the stock for the expected declining cash flow this year.

As of this moment, the dividend is fairly safe. I don’t see imminent danger, but that could change quickly. If cash flow continues to deteriorate as anticipated and the payout ratio keeps climbing, a downgrade is likely – as is a cut.

Dividend Safety Rating: B

What stock’s dividend safety would you like me to analyze next? Leave the ticker in the comments section.

You can also take a look to see whether we’ve written about your favorite stock recently. Just click on the word “Search” at the top right part of the Wealthy Retirement homepage, type in the company name, and hit “Enter.”

Also, keep in mind that Safety Net can analyze only individual stocks, not exchange-traded funds, mutual funds, or closed-end funds.

Where do you get .2475 payout,that was the last quarter. The current quarter due in June is half that!

WU

OWL

tslx

Abr

PDI

NAT please.

IBM please.

ACC or TROWE

Thanks for the update Mark. Would you comment on how the looming fertilizer shortage and other global issues might affect your rating? TIA.

Thoughts on XRAY?

MO

Dog Simon Property Group. Great REIT. Steady stock increases over time while sporting a 4%+ Dividend. It’s a

Safe and secure play.

Thoughts out there?

Mr E.

LHX, L3harris technologies.

IRM

JEPQ, JEPI, AMLP.

VZ – Verizon

Please analyze PMT