People love to pile it on IBM (NYSE: IBM) when things aren’t going well for Big Blue. Critics call the once-dominant computer giant a dinosaur.

I believe they’re wrong. IBM is much more than hardware. Software, cloud services, artificial intelligence and even blockchain technology are all important parts of its business.

It’s why I recommended the stock last November. I was a bit early, which is typical for an investment in a contrarian stock. But a 4.2% yield makes it easier to be patient.

And last week’s strong earnings report was a step in the right direction.

But can investors rely on the dividend while they wait for IBM’s stock to recover?

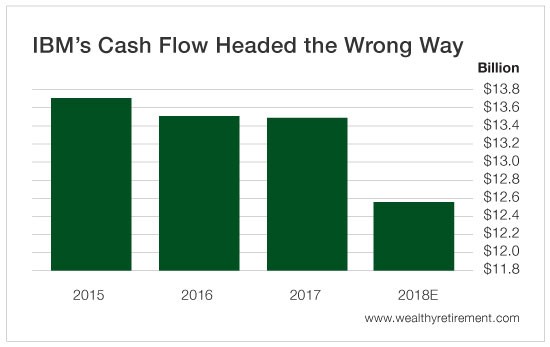

The company’s cash flow has been pretty stagnant lately. It has dipped each of the last two years and is expected to drop 7% in 2018.

Those of us who toil at SafetyNet Pro headquarters don’t like to see charts that are going down to the right. And neither does SafetyNet Pro itself.

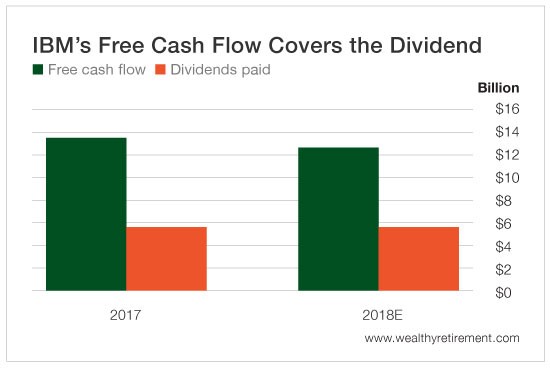

Fortunately there’s another chart that makes us feel better.

As you can see, despite a decline in the cash flow forecast this year, it will easily cover the $5.74 billion in dividends that IBM is expected to pay shareholders. Though we don’t want to see free cash flow fall any further, that 46% payout ratio still leaves plenty of room for the company to pay the dividend and even raise it.

And unless free cash flow falls off a cliff, it’s very likely that IBM will in fact increase the dividend next year. It has done so every year for the past 23 years, including just this past May.

So a low payout ratio and more than two decades of annual dividend hikes tell me that even though free cash flow is not moving in the right direction, this dividend is safe for the foreseeable future.

And should free cash flow start to climb in the future, as I expect it will, look for some big dividend raises in the coming years.

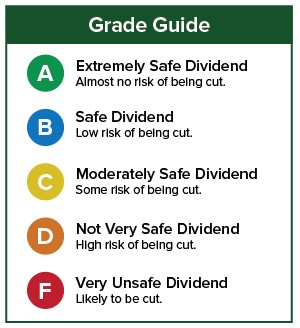

Dividend Safety Rating: A

If you have a stock whose dividend safety you’d like me to analyze, leave the ticker in the comments section.

Good investing,

Marc