The Safest High-Yield Dividend in the World

Marc Lichtenfeld, Chief Income Strategist, The Oxford Club

People are looking for more ways to bring in income in this economy. Many have realized that if they invest in the right dividend-paying stocks, they’ll gain a never-ending stream of money. They’ll be growing their net worth while they sleep.

Right now, there are more than 3,000 publicly traded dividend stocks on the market. But few pay nearly double-digit yields, and even fewer pay high, safe yields.

There are always exceptions, though… like the company in this report.

Rather than inflating the bank accounts of overpaid CEOs and directors, this company pays its excess profits back to its shareholders.

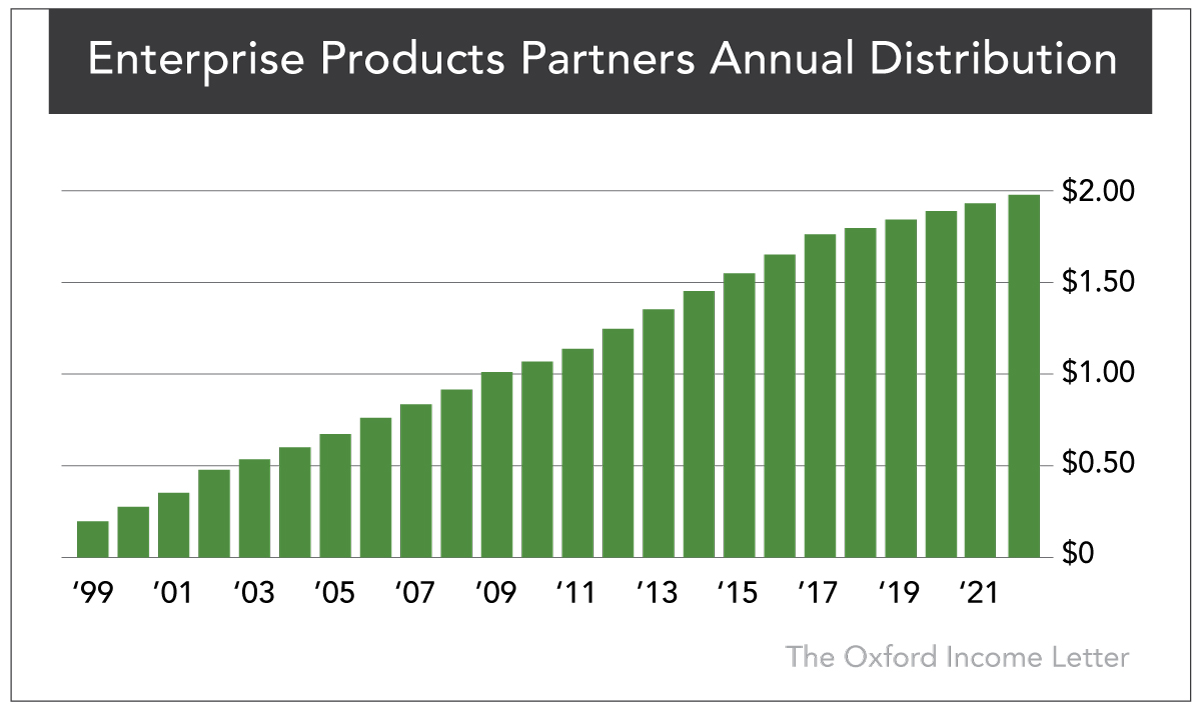

Even better, it just raised its dividend, giving it a over a 7% yield. What’s more, it’s raised this dividend every year since 1998.

Best of all, this company is in a stable industry that is recession-resistant and is set up for incredible growth in the years ahead.

It’s a commodity transportation company – a pipeline operation, primarily – that acts as a toll collector for S&P 500 companies that need to ship their products.

Consider this… Because of the pandemic and economic instability, many businesses, like movie theaters, restaurants and retail stores, were forced to rethink how they operate.

But the one thing people will always need, at least for the foreseeable future, is fuel – specifically, oil and natural gas.

And while a lot of oil and gas producers have had a rough ride as of late, this company makes money no matter who is selling the stuff. Just like a tollbooth attendant, it collects fees to the tune of billions of dollars for transporting fuel through its pipelines.

Furthermore, oil and gas companies, both domestic and foreign, are more than happy to pay the toll. Why? Because building and maintaining their own pipelines would be expensive and inefficient.

But thanks to Enterprise Products Partners (NYSE: EPD), oil and gas companies can deliver their products to Americans across the country at a negligible cost to themselves… which generates substantial profits for the toll collector.

And there’s even more here than meets the eye…

The Gas Must Flow

Founded in 1968 and based in Houston, Texas, Enterprise Products Partners is a premier midstream energy services company.

“Midstream” refers to the fact that the company does not produce oil and gas but stores and transports them to the places where they will be refined. It owns several of the colossal oil and gas pipelines that carry the lifeblood of the modern world.

In all, Enterprise’s portfolio includes more than 50,000 miles of pipelines and over 300 million barrels of storage capacity for NGLs, crude oil, petrochemicals and refined products. Plus, the company has the capacity to store 14 billion cubic feet of natural gas and also operates a number of ports, processing plants and refineries.

As the U.S. economy bounces back, more oil and gas will flow through the company’s pipelines, and the prices of those commodities will rise as well.

And while Enterprise Products Partners doesn’t sell oil and gas, oil and gas prices do affect the company’s stock and the stocks of most master limited partnerships (MLPs).

Because Enterprise is an MLP, its distribution (MLPs pay distributions, not dividends) is tax-deferred, as it is considered a return of capital.

Return of capital is not taxed as income. Instead, it lowers your cost basis and increases your capital gains when you sell the stock.

And that distribution is as juicy as an overripe nectarine. Enterprise Products Partners currently pays a quarterly distribution of $0.54 per unit (MLPs are issued in units, not shares), which comes out to a 7.4% yield on a stock that costs about $30 as of this writing. Again, that’s a 7.4% tax-deferred yield.

The company has now raised its distribution (dividend) for 27 years in a row. It has raised it 18% over the last five years…

Enterprise’s clients include some serious heavy hitters in the oil and gas industry. Major producers like Chevron and Exxon Mobil pay Enterprise to run their product through its pipelines.

With a network that big and friends and allies that powerful, it should come as no surprise that Enterprise has a healthy balance sheet.

In 2021, sales soared to $40.8 billion from $27.2 billion in 2020. Despite the huge growth in 2021… 2022 revenue jumped another 42% to $58.2 billion.

Net income increased 18.4% to $5.49 billion in 2022 from $4.73 billion in 2021.

Even though oil and gas prices were lower in 2023, Enterprise still reported results similar (some metrics were even better) to its outstanding results in 2022.

For the fiscal year 2023 ending December 31, 2023, net income was $5.6 billion or $2.50 per common unit, compared with $5.5 billion or $2.40 per common unit, for the same period in 2022.

OPEC+ production cuts helped raise the price of oil in 2024 leading to more growth for Enterprise. The company reported record net income attributable to common unitholders of $5.9 billion, a 7% increase over fiscal year 2023.

In addition, Enterprise repurchased approximately $219 million of its common units on the open market in 2024. This brings the company’s total common unit repurchases to approximately $1.1 billion. Buybacks increase a stock’s potential growth for shareholders. Large, Strong and Growing.

Enterprise made some big moves recently that greatly expanded its business footprint.

Most notable was the $3.25 billion acquisition of fellow pipeline operator Navitas Midstream Partners. The acquisition adds approximately 1,750 miles of pipelines and over 1 billion cubic feet per day of natural gas processing capacity.

Additional capital investments included $1.4 billion in growth capital projects, $160 million for purchases of pipelines and related assets, and $372 million in sustaining capital expenditures.

On August 21, 2024 Enterprise announced that the company entered into a definitive agreement to acquire Pinon Midstream in a debt-free transaction for $950 million in cash consideration. Pinon Midstream provides natural gas gathering and treating services in the Delaware Basin in New Mexico and Texas. These assets should accelerate Enterprise’s development in the area by at least three years.

It’s a fundamentally strong company that raises its dividend every year. And Enterprise is making more than enough profit to continue expanding the business, make timely share purchases and keep increasing the dividend.

If you act quickly before the global economy recovers, you can lock in over a 7.% yield at a bargain price.

Take advantage of the low price and high yield before Enterprise bounces back.

Action to Take: Buy Enterprise Products Partners (NYSE: EPD) at market. Set a 25% trailing stop to protect your principal and profits.

Big Dividends and Big Potential

Enterprise is the under-the-radar dividend play to make right now.

Between Enterprise’s low payout ratio, its incredible yield and its history of raising its dividend, it really is no wonder that Morningstar recently called Enterprise “compelling and undervalued.”

Enterprise’s leadership believes the company is set up for incredible growth in the coming years.

No matter what 2025 brings with the price of oil and gas… and no matter what happens in the wider world, the oil must flow.

And it will flow through Enterprise’s pipelines while you profit from the tolls.

Enterprise remains my favorite play in the sector. It should be added to your portfolio if you don’t yet own it.