Editor’s Note: I’m grateful for all the lessons my dad has taught me over the years: how to stand up for myself, how to treat people with respect and give them a firm handshake, and even how to whack a golf ball over the pond at the golf course up the street.

He may have regretted that last lesson after I started beating him at golf consistently… but I digress. (Sorry, Dad. I had to say it.)

Below, Chief Income Strategist Marc Lichtenfeld reflects on one of the most important lessons his dad ever taught him about investing.

To all the dads out there, thank you for everything you do, and the entire Oxford Club team wishes you a very happy Father’s Day weekend.

– James Ogletree, Senior Managing Editor

I was thinking about my dad recently. He would have turned 90 at the end of May. I miss him.

He was an incredible role model in how to be a good father, son, husband, brother, and citizen.

He had a lot of interests. He was a sensational musician who could hear a song once and play it note for note on the piano.

He loved basketball too. A lifelong Knicks fan, he would have been thrilled to see them win their first NBA title in 53 years.

One area that he was not particularly skilled or interested in, however, was the stock market.

Ironically, the market was the subject of one of the biggest lessons he ever taught me – and he did so inadvertently.

I was home for a visit, and we were sitting in the basement of the house I grew up in, talking about the stock market. He told me that he’d sold all of his stock investments after the 1987 crash and hadn’t gotten back in until years later, when the 1990s bull market was well underway.

He sold at the bottom and missed out on years’ worth of gains.

At that time, I had just started my career and was working as an assistant on a trading desk. When it came to the markets, I didn’t know nothin’ about nothin’, but his reaction to the volatility in the market stuck with me.

My dad hadn’t behaved differently than millions of investors do when stocks fall. They understandably worry that their money is gone forever. After taking the losses, the scars run so deep that they swear off the market for good.

But then, the next time stocks have run much higher, they feel like they’re missing out, so they get back in.

Rinse and repeat.

The thing is… it makes total sense to be bearish.

There is always something serious to be worried about.

War.

Corruption and idiots in Washington.

Increases in the cost of living.

In fact, you can look back at history and see some truly terrible things that should have sunk the market:

- World War II, the Korean War, and the Vietnam War

- The Cuban Missile Crisis

- The Kennedy assassination

- The high inflation of the 1970s

- Watergate

- The current divisiveness in the U.S.

Those are just a few.

A rational person might look at those things and assume that the market would drop as a result (and not rise again until those issues were resolved).

They’d be wrong. Very wrong.

The opposite is often true too: During bull markets, it’s easy for us to feel like we’re all geniuses and that we’ll never lose money again.

Though the market is doing great right now, eventually, it’s going to turn lower.

You might be thinking, “Thanks, Debbie Downer,” but it’s the truth. That’s how markets work. Bear markets and even the occasional crash are parts of regular cycles.

The circumstances are a little different each time, so it may feel brand-new… but it isn’t.

We’re also a little bit older with a little less time to wait for the eventual rebound, which makes it scarier.

Either way, you don’t want to do what my dad did: sell low and buy high. It will have a negative impact on your wealth.

Here are three simple but important things to remember the next time there’s a sell-off, bear market, or crash.

1. Bear markets have always been followed by new highs.

Always. Without exception.

Now, it may not happen as quickly as you’d like, but it does eventually occur.

People are always innovating, and businesses are always adding new products or services – even in tough times. Investing in a profitable, cash flow-producing company is one of the best ways to grow wealth.

That doesn’t change just because of a sell-off – no matter how nasty it is.

2. Think about your money in “time buckets.”

When do you need cash?

If it’s in the next three years, take that amount out of the market now – not because the market is frothy, but because anything can happen in the short term.

If you need cash in order to pay the mortgage, a college tuition bill, etc., in the next three years, get that money into something very conservative, like a Treasury, CD, or short-term investment-grade corporate bond (not a bond fund − an actual bond).

If your horizon is three to five years for that money, you can mix in some stocks, but I wouldn’t speculate with cash that will definitely be needed within five years. Dividend payers or rock-solid companies mixed with more conservative investments like bonds are a good bet for this time frame.

Remember, bear markets are always followed by new highs, but it can sometimes take a few years.

If your time horizon is longer than five years, more stocks are fine. You still want to invest smartly – and dividend growers are a great way to do just that − but the longer the time frame, the more risk you are able to take.

3. Don’t try to time the market.

Everyone who sells when things are bad says they’ll buy when the market is even lower.

They never do. It’s too scary.

No one ever calls the top accurately or sells as things are just starting to roll over either.

If your money is divided into time buckets as described above, you won’t have to worry too much about the next downturn.

The money you need soon will be immune from lower stock prices, and your intermediate-term funds will mostly be protected as well.

As for your long-term money? A bear market might sting, but you have time on your side.

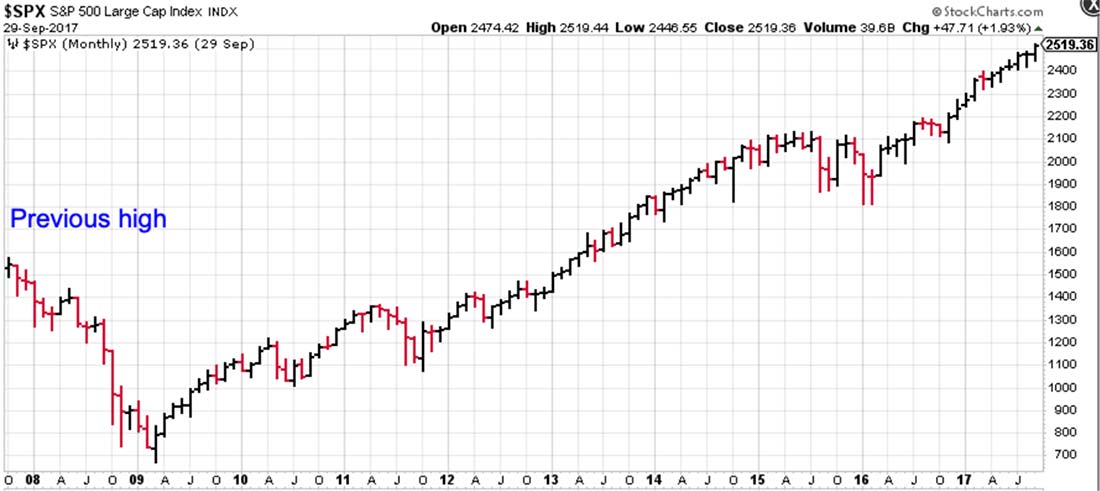

Remember how brutal the global financial crisis was?

The market was back to its previous high in about 5 1/2 years.

That was torture if you needed the money soon, but it wasn’t a big deal if you didn’t need it for 10 years.

Ten years from the high preceding the crisis, the market was up 63%.

I’ve read lots of books on the market (I’ve even written a couple), taken classes, studied for countless hours, and acquired various market-related designations and licenses.

But the lesson that stuck with me the most was when my dad shared his journey with me in the hope that I wouldn’t make the same mistake.

Mission accomplished, Dad.

Thank you.

What are the best lessons – investing-related or not – that you learned from your dad?

Let me know in the comments.

May Dad’s best advise was to never take a second mortgage on your home to create cash to spend.to buy things.

I heeded his advice and after the 2007-2008 housing bubble bust a great deal of folks were losing their homes to foreclosure. It was then I most appreciated his advise.

Greatest advice I have read in a long time Thanks Terry

Growing up my father would tell me that “a msn is only worth what is in his bank account.” So as a teen I worked on the weekends for my father who was a contractor. My brother worked at a restaurant and I was hired to wash dishes, which I would do in my spare time. I graduated from H.S.and enrolled in our local J.C. where I studied to be a fireman.

One day while I was in the administration office I noticed a jobs board, UPS hiring!

I called, and I was hired, so I was now going to college and had three jobs!

I don’t believe that my father’s statement was the best advice, but I wasn’t going to be a young man with nothing in the bank.

Between the three jobs and college, I was not getting much sleep and I knew something had to give. I quit the restaurant job first, and was starting to feel depressed about my life, at least financially. I could work as many hours for my father as I wanted, but it was not what I would choose as a career. After acquiring my fire science degree I thought is this what I really want to be? I did a lot of soul searching and before graduation I needed to take an elective, and I picked a “Personal Finance “class.

I was at my wits end, working grave yard for UPS, going to school in the morning and working for my father between meals and sleep.

It was then that I walked into the “Personal Finance” class and had to sit in the front row because all the others were taken. The professor asked, “who thinks you work harder than everyone else, and nothing can work harder than you.?” I immediately raised my hand and explained what I was doing….he said, “do you work 24 / 7 ?” I said no. He then drew a large $ on the board and said, “ this Mr. Caro works harder than you, it works 24 / 7 “.

It was my first wake-up call about finances.

I decided to make my career with UPS, worked for 36 years, retired at 55 as a manager. I purchased stock, and was involved in their 401k plan, I hypothecated stock to buy more annually and retired with a sizable portfolio.

Today, my wife and I enjoy traveling, and spending vacation with our four children their spouses and eleven grandchildren.

Life is good, we are truly blessed.

Raul Caro

My Dad taught me the key to retirement was diversification and solid dividend paying investments. So he retired (part time) at 62 and myself fully at 61. Thanks Dad, wish you were still here as well.

I had a great (enough) portfolio early in 2008. I wish I’d kept it. I’d be rolling in money!

My father told me,once or twice, “when in doubt sell have,when in doubt buy half, you can always come back when your investment worsens or improves”.

Be very wary of CRE investments. My dad at the 75 years of age was misled by a major investment house to invest in very illiquid CRE LLCs.

My dad always told me “do the best that you can”. This always helped me when I saw others doing better than me and kept me going. Also, when things don’t go quite the way you want, I remembered – do the best that you can. These simple words always stayed with me and I passed them on to my children.

Excellent Marc. Thank you and Happy Father’s day.

MPG

Thanks for sharing Marc

My Dad did not share a lot about his financial world to me. But I do remember one incident that made an impression. He lost about 10K on another persons advise. I always take another’s advise as a grain of salt. If I lose (every investor does) , I lose from my own visions and insights.

When I graduated from college my dad told me to Double Down on the mortgage payments to my first home and to my car. This paid them off quicker, saved Interest (which was very high back then) and started me towards which today is an 800 credit score. As I repeated this process a couple of times I was able to buy a car cash and since that day by Saving what the payment would have been when it’s time to get another car I have money to pay cash for the next one. So in that process from 40 years old I’ve never had a car payment again. The same process worked for me for the last 25 years and now into retirement I have no house payment. So in my retirement two major expenses of home and cars are not in my budget.

This had nothing to do with investing, but a trivia comment for Mark. It your update you mentioned your father “loved basketball “. The game was invented by a Canadian. He was in the US when he invented Basketball.

Minimize personal interest expense. If you have a mortgage, almost always pay it off as quickly as you can. Save and invest for what you want, don’t borrow for items meant for personal gratification.

After asserting that stock markets always rise after bear markets, there is the usual warning to not try to “time the markets”….Well, that would mean not buying things when the market and stocks are very low, even if it is known that they will rise again…And that means passing up the opportunity to buy good stocks in bear markets.